Amazon (AMZN) Analysis 2026: Is the Cloud & AI Giant a Buy?

Amazon (AMZN) is not just a retail giant; it is the operating system of global commerce and internet infrastructure. In 2026, with aggressive investments in Artificial Intelligence and continued dominance in the cloud via AWS, the company stands at a strategic crossroads. With volatile stocks following the Q4 2025 earnings report, is it worth investing now?

Table of Contents

- Who is Amazon and what does it do?

- Quantitative Analysis: The Strength of Numbers

- Qualitative Analysis: Competitive Moats and AI

- Technical Analysis: Buy and Sell Points

- Detailed SWOT Analysis

- Conclusion: The Verdict

- Frequently Asked Questions (FAQ)

Who is Amazon and what does it do?

Founded by Jeff Bezos in 1994 as an online bookstore, Amazon has transformed into a diversified technology conglomerate. Today, the company operates on three main pillars that generate synergistic value:

- Global E-commerce: The world’s largest online retailer (excluding China), with a logistics

network (Fulfillment by Amazon) that rivals dedicated transport companies like FedEx and UPS. - Amazon Web Services (AWS): The group’s “cash cow.” Global leader in cloud computing, providing

infrastructure for millions of startups, corporations, and governments. It is the company’s primary source of

operating profit. - Services and Advertising: Includes Amazon Prime (+200 million subscribers), streaming services

(Prime Video, Twitch), and a digital advertising division that is growing rapidly, challenging the Google-Meta

duopoly.

Quantitative Analysis: The Strength of Numbers (Q4 2025)

Fourth-quarter 2025 results show a company that continues to grow but requires intensive capital to lead the AI race. Total Revenue reached the historic milestone of $213.4 billion (+14% YoY). Below, we detail the performance by segment:

Performance by Product and Service Segment

To understand Amazon, one must look beyond the total number. Each division tells a different story of growth and profitability:

| Segment | Revenue (Q4 2025) | Performance Highlight |

|---|---|---|

| Online Stores (First-Party Retail) | $82.99 Billion | The original pillar remains strong, representing ~39% of total revenue. Solid growth driven by logistical efficiency. |

| Third-Party Seller Services | $42.82 Billion | Services for third-party sellers (commissions, fulfillment) grew faster than first-party retail, showcasing the marketplace’s strength. |

| AWS (Cloud and AI) | $35.6 Billion | Growth of +24% (strong acceleration). Generative AI demand is reheating this sector, which is the most profitable for the company. |

| Advertising Services | $21.3 Billion | The silent “rocket.” Grew +22%, consolidating itself as a digital advertising giant with extremely high margins. |

| Subscription Services | $13.12 Billion | Recurring revenue from Amazon Prime, Audible, and Twitch. Ensures loyalty and predictable cash flow. |

| Physical Stores | $5.86 Billion | Smaller segment (Whole Foods, Amazon Fresh), with stable growth, serving as a base for the omnichannel strategy. |

Financial Highlight: Operating Profit remains robust, largely funded by AWS and Advertising, which offset the tight margins of retail. The projected Capex of $200 billion for 2026 reflects the massive bet on AI infrastructure (Data Centers and Chips).

Qualitative Analysis: Competitive Moats and AI

Competitive Advantages (Moats)

- Network Effect (Marketplace): More sellers mean more products; more products mean more

customers. This virtuous cycle, combined with 3P services ($42.8 bn), creates an almost insurmountable barrier. - Switching Cost (AWS): Once a company builds its infrastructure on AWS, migrating to Azure or

Google Cloud is costly, technical, and risky. Loyalty here is structural. - Logistics: Prime’s “Next-Day” or “Same-Day” delivery created a convenience standard that few

competitors can match on a global scale.

The Bet on AI (Bedrock and Chips)

Andy Jassy, Amazon’s CEO, doubled down on AI. The company is not only selling access to third-party models (via Amazon Bedrock) but developing its own AI chips (Trainium and Inferentia) to reduce dependence on Nvidia and lower costs for customers.

Technical Analysis: Buy and Sell Points

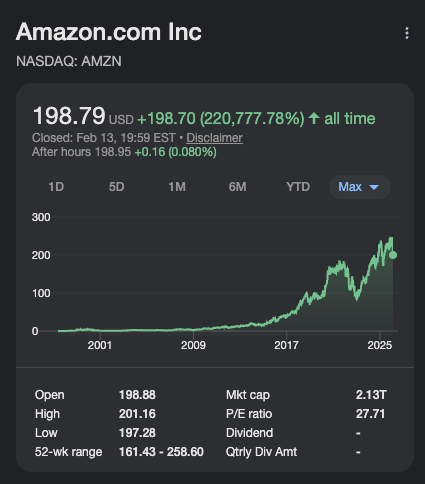

In February 2026, AMZN stock faces technical volatility, trading in the $198 – $205 range, following a post-earnings correction.

- Trend: Short-term sideways/correction; Long-term Bull Market (Secular).

- Strong Support: $197 – $200 (Lower Bollinger Band and price memory). Losing this level could

lead the stock to test $185. - Immediate Resistance: $205 (20-period Moving Average).

- Key Resistance: $240 (Recent historical highs).

The RSI (Relative Strength Index) near oversold regions suggests that the current discount could be an interesting entry opportunity for investors with a long-term horizon.

Detailed SWOT Analysis

Strengths

- Global leadership in Cloud (AWS) and E-commerce.

- Prime Ecosystem (+200m subscribers).

- Revenue diversification (Ads, Cloud, Retail).

- Massive investment capacity (Capex).

Weaknesses

- Low margins in online retail.

- Dependence on third-party sellers creates quality risks.

- Gigantic operational complexity.

Opportunities

- Explosive expansion of Generative AI in AWS.

- Ad monetization on Prime Video.

- Robotics and logistics automation reducing costs.

- Health (Amazon Clinic) and B2B Market.

Threats

- Antitrust Actions (FTC/EU) seeking to break up the company.

- Predatory competition (Temu, Shein, TikTok Shop).

- Rapid advancement of Microsoft (Azure) in AI.

The Verdict

Amazon remains one of the most robust investment theses in the world. The recent drop in shares reflects market fear regarding increased spending, but history shows that Amazon knows how to allocate capital to create competitive moats. The accelerated growth of AWS and Advertising are powerful profit engines.

For the long-term investor, prices below $200 seem like an attractive entry point. The company is sacrificing today’s profits to dominate tomorrow’s AI — exactly the strategy (Day 1) that made it a trillion-dollar giant.

Frequently Asked Questions (FAQ)

1. Does Amazon pay dividends?

No. Amazon historically reinvests all its profit into business growth and share buybacks.2. What is AWS and why is it important?

AWS (Amazon Web Services) is the cloud division. It is crucial because it generates most of the operating profit, funding other areas.3. Who are the biggest competitors?

Retail: Walmart, Alibaba, Shein. Cloud: Microsoft, Google. Streaming: Netflix.4. Will AI help Amazon?

Yes. It boosts AWS (infrastructure for AI), improves logistics, and ad personalization.5. Why did the stock drop in early 2026?

Due to the announcement of aggressive Capex increase ($200 bn) for 2026, reducing free cash flow expectations.Disclaimer

This article is strictly educational. It does not constitute a recommendation to buy or sell. The stock market involves risks. Conduct your own analysis.

References

- Amazon Investor Relations (Q4 2025 Earnings Release).

- Market Reports: Morningstar, The Motley Fool, Investing.com.

- Technical Data: TradingView and ChartDepth.